We've finally gotten to a point where I think all data series have had some level of explanation or are at least straightforward enough that we can cut right through them. In any case, the data this week were somewhat of a mixed bag, though still show that the economic recovery remains intact. Without further ado:

April New and Existing Home Sales

As expected both new and existing home sales had very strong months in April. New home sales were up 14.8% at an annual rate and existing home sales were up 7.6%. However, this was largely due to the homebuyer tax credit. As we have discussed previously, that is likely to distort the data going forward for some time to come. How much the distortion will be has yet to be seen, but my guess is that it will be significant. The depressed home sales in the coming months will probably weigh on prices that have otherwise firmed recently, which takes us to our next data...

March S&P Case Shiller House Price Index

Sputtering. That is the appropriate word to use for what had been some decent house price increases in mid through late 2009. Seasonally adjusted, house prices did edge up somewhat in March in the markets followed by the 10-city index, but the broader 20-city index fell slightly from 146.0 to 145.93. Not a huge decline, but still it does indicate that house prices are likely to remain moribund for some time to come.

Monday, May 31, 2010

Friday, May 28, 2010

End of Month Open Thread

Well, it's been quite a month for the markets and I hope that those of you who were unfamiliar with financial markets have learned something here. This open thread is a chance to share your thoughts, experiences, suggestions, or whatever else you feel like.

Thursday, May 27, 2010

Threading Strategies Together

Several different strategies have been discussed here on Finance Monitor along with numerous individual investments and I thought I would provide some context on how to view the discussions in the context of your own investments. The fundamental goal of this post is to weave several different posts on different subjects together. I will try to provide links so that you can quickly look up the prior discussions.

I guess the proper way to start this conversation was with the prior post on risk reduction in portfolio construction. This is one way of looking at your macro strategy, though there are many potential variations on this broader strategy. Within the core portfolio, either use equity index funds or balanced funds and basically just try to keep your overall allocation right, unless you want to be a little more active here. Then, you can engage in what was discussed on the post on dynamic asset allocation.

To do this, use the SPY and TLT ETFs at a basic level. If you have less than $2,000, I strongly encourage you to only re-balance when interest rates suggest you make a large reallocation from stocks to bonds or bonds to stocks. If you re-balance with every twinge, you'll get eaten alive by commissions. For example, let's say the model changes each month and you re-balance with $7 commissions each time (on both purchase and sale) with a $2,000 balance. You will incur $14 a transaction 12 times for a total of $168 in commissions. That would be 8.4% of your portfolio or greater than your average annual gain. With $20,000, it's 0.84%, which is bad, but not ruinous. If you are so fortunate to get up to $100,000, the fees are very low indeed. The ETF fees for TLT and SPY are also very low. In the case of SPY they are 0.09% per year and 0.15% on TLT.

I guess the proper way to start this conversation was with the prior post on risk reduction in portfolio construction. This is one way of looking at your macro strategy, though there are many potential variations on this broader strategy. Within the core portfolio, either use equity index funds or balanced funds and basically just try to keep your overall allocation right, unless you want to be a little more active here. Then, you can engage in what was discussed on the post on dynamic asset allocation.

To do this, use the SPY and TLT ETFs at a basic level. If you have less than $2,000, I strongly encourage you to only re-balance when interest rates suggest you make a large reallocation from stocks to bonds or bonds to stocks. If you re-balance with every twinge, you'll get eaten alive by commissions. For example, let's say the model changes each month and you re-balance with $7 commissions each time (on both purchase and sale) with a $2,000 balance. You will incur $14 a transaction 12 times for a total of $168 in commissions. That would be 8.4% of your portfolio or greater than your average annual gain. With $20,000, it's 0.84%, which is bad, but not ruinous. If you are so fortunate to get up to $100,000, the fees are very low indeed. The ETF fees for TLT and SPY are also very low. In the case of SPY they are 0.09% per year and 0.15% on TLT.

Tuesday, May 25, 2010

Interesting Perspective on Bottom Fishing in Europe

There's a good Wall Street Journal article about the dangers of some of the more popular European ETFs. The principal issue that the authors highlight is that these indexes may be too heavily tilted toward the banks. As someone who lost a fair amount of money on bank stocks during the worst of our financial crisis, I am more discerning about bottom fishing than I used to be, so this caught my attention.

I still think there might be some money to be made in the broad ETFs like EWP, but indeed the better way to play this rout of European stocks is to look for the companies least effected by the crisis, but that have gotten destroyed anyway. The article mentions Telefonica (TEF), which has gotten absolutely clobbered and now yields over 8% with an 8-9 PE, depending on which earnings estimates you use. That's not bad and also Telefonica is unlikely to suffer severe damage. Communications outlays are not as vulnerable as other forms of consumer discretionary spending.

The same goes for stocks here. United Technologies (UTX) is down from $77 to $66 and it really isn't that likely to be effected by primary, secondary, or even tertiary effects of the European crisis.

What do you all think? Does this view make sense to you?

I still think there might be some money to be made in the broad ETFs like EWP, but indeed the better way to play this rout of European stocks is to look for the companies least effected by the crisis, but that have gotten destroyed anyway. The article mentions Telefonica (TEF), which has gotten absolutely clobbered and now yields over 8% with an 8-9 PE, depending on which earnings estimates you use. That's not bad and also Telefonica is unlikely to suffer severe damage. Communications outlays are not as vulnerable as other forms of consumer discretionary spending.

The same goes for stocks here. United Technologies (UTX) is down from $77 to $66 and it really isn't that likely to be effected by primary, secondary, or even tertiary effects of the European crisis.

What do you all think? Does this view make sense to you?

Monday, May 24, 2010

Event Risk: Thy Name is Korea

For those not familiar with the terminology, "event risk" is a fairly simple concept and I am almost ashamed to use the term because of its simplicity. It simply means that there is the risk that a major event outside of regular market forces will shake a specific company or even an entire market. For example, BP's event risk has been the ongoing oil spill. Simple enough concept.

With that out of the way, let's move on to South Korea and the escalating crisis with the North over the sinking by the North of a South Korean naval vessel. This is yet another instance of where one must pay attention to politics when making investment decisions. South Korea is an attractive market in a number of ways. The government is fiscally stable, the economy is clearly in a high growth mode, companies are becoming increasingly profitable, and China provides a great long term driver of export growth. There's an awful lot to like. However, they do have an absolutely berserk neighbor to the north.

However, as serious as this crisis seems, it is not clear that the Korean markets have taken the risk as seriously as one might think.

Against EEM, an overall emerging markets index ETF, EWY, the South Korean iShares ETF, has not done that much worse, certainly not so much worse as to indicate broad investor skittishness. Compared to the potential for ruin the South Korean economy should a war commence, this response seems modest. Of course, even when U.S. markets became aware of the Cuban Missile Crisis, stocks did not sell off particularly fiercely either. Maybe markets generally are fairly unimpressed by political (broadly defined) turmoil. Even in Thailand, ongoing political violence has barely dented the market lately.

Against EEM, an overall emerging markets index ETF, EWY, the South Korean iShares ETF, has not done that much worse, certainly not so much worse as to indicate broad investor skittishness. Compared to the potential for ruin the South Korean economy should a war commence, this response seems modest. Of course, even when U.S. markets became aware of the Cuban Missile Crisis, stocks did not sell off particularly fiercely either. Maybe markets generally are fairly unimpressed by political (broadly defined) turmoil. Even in Thailand, ongoing political violence has barely dented the market lately.

So, why the post title indicating that South Korea is a poster child for event risk? I would say it is because if what South Korea is facing isn't event risk, I don't know what is. And if this is major event risk, why is the market not more concerned than it is? Am I reading the situation entirely incorrectly?

Also, if anyone has any special insights on the ongoing Korean tensions, I'd be happy to hear them. There might be some money to make here for those that fancy investing in Korea.

With that out of the way, let's move on to South Korea and the escalating crisis with the North over the sinking by the North of a South Korean naval vessel. This is yet another instance of where one must pay attention to politics when making investment decisions. South Korea is an attractive market in a number of ways. The government is fiscally stable, the economy is clearly in a high growth mode, companies are becoming increasingly profitable, and China provides a great long term driver of export growth. There's an awful lot to like. However, they do have an absolutely berserk neighbor to the north.

However, as serious as this crisis seems, it is not clear that the Korean markets have taken the risk as seriously as one might think.

So, why the post title indicating that South Korea is a poster child for event risk? I would say it is because if what South Korea is facing isn't event risk, I don't know what is. And if this is major event risk, why is the market not more concerned than it is? Am I reading the situation entirely incorrectly?

Also, if anyone has any special insights on the ongoing Korean tensions, I'd be happy to hear them. There might be some money to make here for those that fancy investing in Korea.

Sunday, May 23, 2010

Economic Data Summary: Week Ending May 21st, 2010

The data released in the past week were mixed, the first week in a while where that was true, however there does not seem to be much of a change in the overall trend of steady, moderate economic growth.

April Consumer Price Index (CPI)

This is the measure of prices paid by consumers for a pre-determined basket of market goods. Along with the PCE deflator, it is one of the two primary methods for determining the rate of inflation for consumers.

In April, the headline number fell 0.1% and is up 2.2% year on year. The April decline was driven by lower energy prices and that trend will probably continue for a couple more months with the recent decline in crude oil prices as well as gasoline and natural gas prices. The core rate, less food and energy, was flat for the month and is up 0.9% year on year. Inflation is very modest and there are few signs that it will accelerate soon in any meaningful way.

April Producer Price Index (PPI)

This is essentially the CPI for businesses, focusing on manufacturers in particular. There's really not much more to say about it except to say that, along with the CPI, these releases can move markets when there are concerns about Federal Reserve interest rate moves. This is because when markets are on edge fearing rate hikes, strong inflation numbers will change interest rate expectations to the upside and hurt equity and bond prices.

Like the CPI, the headline number was down 0.1% month on month, driven by energy. Year on year, the finished goods index was up 5.5%, which would look scary under most circumstances. However, as recently as July of last year the PPI was down 6.9% year on year so the comparisons are somewhat skewed. PPI is subject to much more wild swings than CPI because changes in raw materials prices are felt more rapidly and are not moderated by the fact that not all price increases are passed on to consumers.

April Housing Starts

April Consumer Price Index (CPI)

This is the measure of prices paid by consumers for a pre-determined basket of market goods. Along with the PCE deflator, it is one of the two primary methods for determining the rate of inflation for consumers.

In April, the headline number fell 0.1% and is up 2.2% year on year. The April decline was driven by lower energy prices and that trend will probably continue for a couple more months with the recent decline in crude oil prices as well as gasoline and natural gas prices. The core rate, less food and energy, was flat for the month and is up 0.9% year on year. Inflation is very modest and there are few signs that it will accelerate soon in any meaningful way.

April Producer Price Index (PPI)

This is essentially the CPI for businesses, focusing on manufacturers in particular. There's really not much more to say about it except to say that, along with the CPI, these releases can move markets when there are concerns about Federal Reserve interest rate moves. This is because when markets are on edge fearing rate hikes, strong inflation numbers will change interest rate expectations to the upside and hurt equity and bond prices.

Like the CPI, the headline number was down 0.1% month on month, driven by energy. Year on year, the finished goods index was up 5.5%, which would look scary under most circumstances. However, as recently as July of last year the PPI was down 6.9% year on year so the comparisons are somewhat skewed. PPI is subject to much more wild swings than CPI because changes in raw materials prices are felt more rapidly and are not moderated by the fact that not all price increases are passed on to consumers.

April Housing Starts

"In Defense of the Humble Balanced Portfolio" - Morningstar

I stumbled across this good article from Morningstar "In Defense of the Humble Balanced Portfolio". This relates to a previous discussion on overall investment strategies and several subsequent posts on asset allocations and portfolio construction.

Incidentally, they do note some shortcomings of a simple static 50/50 stock and bond mix, or any static ratio for that matter, which is what prompted me to work on the dynamic asset allocation model over the past year or so. Even the automatic rebalancing target date funds have their problems as they rebalance at linear rates that may not be opportune given market cycles. That's why I prefer the dynamic, interest rate signal approach.

What do you all think?

Incidentally, they do note some shortcomings of a simple static 50/50 stock and bond mix, or any static ratio for that matter, which is what prompted me to work on the dynamic asset allocation model over the past year or so. Even the automatic rebalancing target date funds have their problems as they rebalance at linear rates that may not be opportune given market cycles. That's why I prefer the dynamic, interest rate signal approach.

What do you all think?

Saturday, May 22, 2010

Is BP a good buy at these levels?

Disclaimer: I am in no way trying to diminish the environmental damages to the Gulf Coast. In fact, I am more than outraged about it. However, remember that on this blog we play the role of cold, Ayn Rand-like, cynical capitalists.

Whenever there is a company just getting its ass handed to it (that's a technical term) like BP (BP) is, there is always some appeal in possibly nibbling at it. Indeed, BP has gotten absolutely slaughtered over the past several weeks.

Compared to the other integrated oil companies, like Exxon Mobil (XOM) and ConocoPhillips (COP), it has been downright ugly.

Compared to the other integrated oil companies, like Exxon Mobil (XOM) and ConocoPhillips (COP), it has been downright ugly.

That being said, it is unclear exactly what the damages to BP will be. If the losses will be only in the range of a few billion dollars, then they're very cheap right now. If, on the other hand, they get hit with $40, $50, or $60 billion in damages and punitive fines, then they're not so cheap. Given that this is an election year and politicians love issues like this because they make for great righteous indignation and extreme sweeping measures, it's anyone's guess.

I personally say no to this because I am risk averse and I don't like the size of the unknowns here. There is the possibility that BP is barred from future exploration and development, for example. However, disagreement is what makes a market. What do you all think?

Whenever there is a company just getting its ass handed to it (that's a technical term) like BP (BP) is, there is always some appeal in possibly nibbling at it. Indeed, BP has gotten absolutely slaughtered over the past several weeks.

That being said, it is unclear exactly what the damages to BP will be. If the losses will be only in the range of a few billion dollars, then they're very cheap right now. If, on the other hand, they get hit with $40, $50, or $60 billion in damages and punitive fines, then they're not so cheap. Given that this is an election year and politicians love issues like this because they make for great righteous indignation and extreme sweeping measures, it's anyone's guess.

I personally say no to this because I am risk averse and I don't like the size of the unknowns here. There is the possibility that BP is barred from future exploration and development, for example. However, disagreement is what makes a market. What do you all think?

Q: How do I value stocks anyway? A: Umm....

One of the basic questions that is brought up time and again is: Is the stock market overvalued or undervalued? Investors are chronically asking this question and the debate between the two factions is what creates a market. Those who think their stocks have had their run will sell and those that think that those stocks can continue to run will buy and where the two meet is the price of the stock. The question for you is which side of that trade do you come down on?

I wish there was an easy answer here, but there is no easy answer. I don't subscribe to any one view of it. Efficient market theorists insist that the price of a stock is always justified because that is what the market values it at. Well.... that's nice, but kind of useless. Then, to quote Cheech Marin's character at the end of From Dusk Till Dawn, "One place's just as good as another". Put in terms of market history, buying Microstrategy (MSTR) at $3,000 a share in March of 2000 made just as much sense as buying Ford (F) at $1 in late 2008.

Dismissing this idea for a moment, how then should stocks, or the stock market at large, be valued? One idea for the overall market is by relative valuation. This is the previously mentioned earnings yield (1/PE * 100%) and compare it to long term bonds. If the earnings yield is at 5% and the 10-year Treasury Note is at 3.5%, stocks seem cheap. If the earnings yield is at 4% and the 10-year Treasury Note is at 7%, stocks are horrifically overvalued. There are some problems with this method in that it is possible that the "E", or earnings, in the PE ratio may be temporarily distorted. Also, interest rates can change in a hurry. It is not uncommon for long term rates to move 100 basis points in a six week period.

If you have taken a microeconomics class that has discussed financial markets at all, or any finance class, you have heard of the Dividend Discount Model. There are two problems with this as well. One is that many companies do not pay dividends, or do not pay particularly large dividends as a matter of policy. As a result, these companies get the shaft in this method of valuation. Also, you have to make the leap of faith that some given level of dividend growth will be sustainable. Just because a company has grown dividends at 8% each year for the past ten years does not mean that they will continue to do so. Case in point: the financials during the 2007-2008 period. If you valued those companies with the assumption that their current dividends were a good proxy of their dividends over the next five years, you would get hosed. Purely conceptually, however, this is probably the best method. It's just that it is difficult to apply to a large number of stocks.

I wish there was an easy answer here, but there is no easy answer. I don't subscribe to any one view of it. Efficient market theorists insist that the price of a stock is always justified because that is what the market values it at. Well.... that's nice, but kind of useless. Then, to quote Cheech Marin's character at the end of From Dusk Till Dawn, "One place's just as good as another". Put in terms of market history, buying Microstrategy (MSTR) at $3,000 a share in March of 2000 made just as much sense as buying Ford (F) at $1 in late 2008.

Dismissing this idea for a moment, how then should stocks, or the stock market at large, be valued? One idea for the overall market is by relative valuation. This is the previously mentioned earnings yield (1/PE * 100%) and compare it to long term bonds. If the earnings yield is at 5% and the 10-year Treasury Note is at 3.5%, stocks seem cheap. If the earnings yield is at 4% and the 10-year Treasury Note is at 7%, stocks are horrifically overvalued. There are some problems with this method in that it is possible that the "E", or earnings, in the PE ratio may be temporarily distorted. Also, interest rates can change in a hurry. It is not uncommon for long term rates to move 100 basis points in a six week period.

If you have taken a microeconomics class that has discussed financial markets at all, or any finance class, you have heard of the Dividend Discount Model. There are two problems with this as well. One is that many companies do not pay dividends, or do not pay particularly large dividends as a matter of policy. As a result, these companies get the shaft in this method of valuation. Also, you have to make the leap of faith that some given level of dividend growth will be sustainable. Just because a company has grown dividends at 8% each year for the past ten years does not mean that they will continue to do so. Case in point: the financials during the 2007-2008 period. If you valued those companies with the assumption that their current dividends were a good proxy of their dividends over the next five years, you would get hosed. Purely conceptually, however, this is probably the best method. It's just that it is difficult to apply to a large number of stocks.

Endowment Losses

I just read an interesting article

http://www.insidehighered.com/news/2010/05/21/endowments

The part I found most interesting was the table showing losses. It might be comforting to know that Harvard, with a team of experts, still lost a lot during the recession.

http://www.insidehighered.com/news/2010/05/21/endowments

The part I found most interesting was the table showing losses. It might be comforting to know that Harvard, with a team of experts, still lost a lot during the recession.

Thursday, May 20, 2010

Strategy Sessions - Part 2: Building Your Portfolio to Protect Your Assets

As I have previously mentioned, there is somewhat of a trade off between the potential, and I will emphasize potential, for high returns and the volatility that you will incur. This relationship is not absolute as, for example, adding some stocks to an all bond portfolio actually reduces your volatility over time. However, it is a fair starting point for considering how to construct your portfolio. All of the following is based off of my own personal views and does not necessarily represent "best practices" in the industry.

Regardless of your volatility preferences, any portfolio should start with a core position or positions. Depending on how much you have to invest and whether or not you meet investment minimums, this position can either be an broad market index fund (S&P 500, Wilshire 5000, or something that tracks a global index like the FTSE All World Index) or a similar ETF. Balanced funds (a mix of stocks and bonds) are also a good choice for core portfolio holdings. If you don't meet minimum investment requirements from your desired mutual fund (ie Vanguard often has a $3,000 minimum), then I say go the ETF route. You also will have greater flexibility in changing ETFs than you will with conventional mutual funds. Just keep an eye on fees. For a small portfolio (<5,000), core positions should be the bulk of what you have. For larger portfolios, core positions can be as little as 25%, in my view.

A quick aside, on fees, you should never pay loads (up front fees) on your mutual funds and keep an eye on expense ratios. If you are paying over 0.80% in annual fees, reconsider your position. Just a .40% differential on fees can cost you 16% in long term returns. Put another way, if you would have had $100,000 in your fund at retirement, you will have $84,000. You want those extra $16,000, so keep your eye on fees.

The next layer of your portfolio can venture out a bit into more volatile, but not crazy investments. Along the fund route, these are things like sector funds that track individual market sectors you think will do well, or broad basket emerging market funds or their equivalent ETFs (EEM, for example). This can also be composed of a basket of positions in various blue-chip companies if you choose to use individual stocks. If the core portfolio is your castle, this is your outer wall. I don't know exactly what to call this, so I will go with meso-portfolio. You have your core portfolio, then your meso-portfolio. I like the scientific sound of it.

From there, you can build your exploratory positions. These can be specific country or region emerging market funds, mid and small cap stocks (provided that they have decent analyst coverage), and so on. The larger your portfolio, the larger these positions can be.

Regardless of your volatility preferences, any portfolio should start with a core position or positions. Depending on how much you have to invest and whether or not you meet investment minimums, this position can either be an broad market index fund (S&P 500, Wilshire 5000, or something that tracks a global index like the FTSE All World Index) or a similar ETF. Balanced funds (a mix of stocks and bonds) are also a good choice for core portfolio holdings. If you don't meet minimum investment requirements from your desired mutual fund (ie Vanguard often has a $3,000 minimum), then I say go the ETF route. You also will have greater flexibility in changing ETFs than you will with conventional mutual funds. Just keep an eye on fees. For a small portfolio (<5,000), core positions should be the bulk of what you have. For larger portfolios, core positions can be as little as 25%, in my view.

A quick aside, on fees, you should never pay loads (up front fees) on your mutual funds and keep an eye on expense ratios. If you are paying over 0.80% in annual fees, reconsider your position. Just a .40% differential on fees can cost you 16% in long term returns. Put another way, if you would have had $100,000 in your fund at retirement, you will have $84,000. You want those extra $16,000, so keep your eye on fees.

The next layer of your portfolio can venture out a bit into more volatile, but not crazy investments. Along the fund route, these are things like sector funds that track individual market sectors you think will do well, or broad basket emerging market funds or their equivalent ETFs (EEM, for example). This can also be composed of a basket of positions in various blue-chip companies if you choose to use individual stocks. If the core portfolio is your castle, this is your outer wall. I don't know exactly what to call this, so I will go with meso-portfolio. You have your core portfolio, then your meso-portfolio. I like the scientific sound of it.

From there, you can build your exploratory positions. These can be specific country or region emerging market funds, mid and small cap stocks (provided that they have decent analyst coverage), and so on. The larger your portfolio, the larger these positions can be.

A Brief Note on Financial Crises and Safe Harbors

One of the great new contrarian pieces of "knowledge" has been that you can hide from a developed market financial crisis in emerging markets. This was said in 2007 and 2008 when we went into the soup and it was said again this time during the ongoing European financial crisis. Just to show how silly that idea is, here is a chart from June 1, 2008 through March 1, 2009:

The green candlestick line is the S&P 500, the olive line is the FXI from yesterday, the purple line is the iShares MSCI Emerging Markets Index Fund (EEM) and the light blue line is the iShares Brazilian Index Fund (EWZ). As you can see, over this period, the U.S. outperformed all of those markets for the duration of the worst of the crisis.

Similarly, in the current crisis the pattern has been continued:

The pattern is repeated, to varying degrees. So, what is the safe harbor? U.S. Treasuries have been, are, and will likely continue to be the last best hope for investors in the midst of a crisis. I could show the chart from 2008, but that's just beating a dead horse. Here's the most recent performance with the iShares Barclay's 20+ Year Treasury Bond Fund (TLT) represented by the.... I guess that's salmon colored line:

As you can see, long-duration U.S. Treasuries are a good safe harbor for assets in short term financial crises, regardless of whether they are here in the U.S. or if they are in Greece, China, Japan, or wherever else there might be a crisis. That being said, as a long term prospect, I am not thrilled with the outlook for Treasuries at the moment as I have indicated previously. As interest rates rise in the future, you will get slaughtered for a large position in them. In the short run they might be appealing, though even here I'm not sure how much more upside they have. I think we are probably within a couple weeks of the worst of the European crisis being behind us, though it will get ugly before it is over.

Someone may ask "What about gold?". In response I say, "Treasuries > gold" in a crisis. It was true in 2008. It is true now. Gold is only superior in a time of hyperinflation.

Anyway, those are my thoughts.

The green candlestick line is the S&P 500, the olive line is the FXI from yesterday, the purple line is the iShares MSCI Emerging Markets Index Fund (EEM) and the light blue line is the iShares Brazilian Index Fund (EWZ). As you can see, over this period, the U.S. outperformed all of those markets for the duration of the worst of the crisis.

Similarly, in the current crisis the pattern has been continued:

The pattern is repeated, to varying degrees. So, what is the safe harbor? U.S. Treasuries have been, are, and will likely continue to be the last best hope for investors in the midst of a crisis. I could show the chart from 2008, but that's just beating a dead horse. Here's the most recent performance with the iShares Barclay's 20+ Year Treasury Bond Fund (TLT) represented by the.... I guess that's salmon colored line:

As you can see, long-duration U.S. Treasuries are a good safe harbor for assets in short term financial crises, regardless of whether they are here in the U.S. or if they are in Greece, China, Japan, or wherever else there might be a crisis. That being said, as a long term prospect, I am not thrilled with the outlook for Treasuries at the moment as I have indicated previously. As interest rates rise in the future, you will get slaughtered for a large position in them. In the short run they might be appealing, though even here I'm not sure how much more upside they have. I think we are probably within a couple weeks of the worst of the European crisis being behind us, though it will get ugly before it is over.

Someone may ask "What about gold?". In response I say, "Treasuries > gold" in a crisis. It was true in 2008. It is true now. Gold is only superior in a time of hyperinflation.

Anyway, those are my thoughts.

Wednesday, May 19, 2010

Investing in China: Now, Later, or Never?

I will preface this entire discussion by saying I am not an expert on China. I do not know a word of Mandarin (or Cantonese for that matter), I do not know the names of more than 25 Chinese companies, and I have never been there. I do, however, know a fair amount about Chinese history and Chinese economic development. As there are a few of you that know more about certain aspects of China, I welcome your input.

Of course, when any economy is growing 11% a year, there is a great temptation to want to invest in that country's markets. With China, where the economic prospects seem so favorable, this is particularly true. However, historically the Chinese stock market has proved a treacherous mistress. For most of the ten years leading up to 2006, Chinese stocks, measured by the CSI 300, did not do particularly much of anything even while the economy boomed. Then, between 2006 and early-2008, Chinese stocks increased nearly six fold, one of the most powerful rallies by a major economy's markets in history. Then, over the next ten months, stocks fell 73%, wiping out most of the gains of the past three years. Over the ten months from October 2008 to August 2009, stocks rallied by better than 100%, out-pacing most other markets.

Since then, however, China has been an unusually poorly performing market, even rivaling some of the troubled European markets. The CSI 300 has fallen from 3,750 in August to 2,762 now, making it one of the few bear markets anywhere in the world. Its best proxy listed here, the iShares FTSE/Xinhua China 25 Fund (FXI), has badly trailed the S&P 500 over

the past year. Despite all of the talk about China being a better place to invest, the

markets have said otherwise:

Of course, when any economy is growing 11% a year, there is a great temptation to want to invest in that country's markets. With China, where the economic prospects seem so favorable, this is particularly true. However, historically the Chinese stock market has proved a treacherous mistress. For most of the ten years leading up to 2006, Chinese stocks, measured by the CSI 300, did not do particularly much of anything even while the economy boomed. Then, between 2006 and early-2008, Chinese stocks increased nearly six fold, one of the most powerful rallies by a major economy's markets in history. Then, over the next ten months, stocks fell 73%, wiping out most of the gains of the past three years. Over the ten months from October 2008 to August 2009, stocks rallied by better than 100%, out-pacing most other markets.

Since then, however, China has been an unusually poorly performing market, even rivaling some of the troubled European markets. The CSI 300 has fallen from 3,750 in August to 2,762 now, making it one of the few bear markets anywhere in the world. Its best proxy listed here, the iShares FTSE/Xinhua China 25 Fund (FXI), has badly trailed the S&P 500 over

the past year. Despite all of the talk about China being a better place to invest, the

markets have said otherwise:

Tuesday, May 18, 2010

Goldman Sachs: Good at making money for themselves. Their clients... not so much

There is a very interesting story from Bloomberg. This is somewhat outside the purview of this blog, but still it is an interesting story that should warn people against listening to what the big firms have to say.

I guess the other piece of advice I have for all of those who consider themselves beginners and don't know this, always read Bloomberg every morning, afternoon, and evening. It is far and away the best financial coverage out there, particularly when you want some coverage of foreign markets.

I guess the other piece of advice I have for all of those who consider themselves beginners and don't know this, always read Bloomberg every morning, afternoon, and evening. It is far and away the best financial coverage out there, particularly when you want some coverage of foreign markets.

Sunday, May 16, 2010

Economic Data Summary: Week Ending May 14th, 2010

The economic data this week were once again fairly positive so the general story of a moderately strong economic recovery remains in place. I will editorialize a bit here to say that compared to the expectations of many 8-12 months ago, we are having a much stronger recovery than projected.

April Industrial Production

My personal favorite coincident indicator as it is the proxy for determining the demand for goods. Manufacturers will not produce if they do not think that there is a market for their goods. The one wrinkle in this is that inventory trends can be a short term driver of the industrial production index, making it unclear how much growth is due to restocking of inventories and how much is actually because of growing end-demand. Industrial production is released by the Fed right about the middle of the month every month.

In line with what we have been seeing out of the manufacturing diffusion indices, industrial production showed strong growth in April with 0.8% growth on the headline number. Below the surface, business equipment grew 1.0% and construction supplies 2.8%. March and January were revised higher, February lower. The diffusion indices also showed broad based growth.

Here's a look at the manufacturing index subset (does not include utilities and mining):

Yes, we are still far below the peak, but the pattern of recovery remains firmly intact. There are not even signs of wheezing at this moment.

April Industrial Production

My personal favorite coincident indicator as it is the proxy for determining the demand for goods. Manufacturers will not produce if they do not think that there is a market for their goods. The one wrinkle in this is that inventory trends can be a short term driver of the industrial production index, making it unclear how much growth is due to restocking of inventories and how much is actually because of growing end-demand. Industrial production is released by the Fed right about the middle of the month every month.

In line with what we have been seeing out of the manufacturing diffusion indices, industrial production showed strong growth in April with 0.8% growth on the headline number. Below the surface, business equipment grew 1.0% and construction supplies 2.8%. March and January were revised higher, February lower. The diffusion indices also showed broad based growth.

Here's a look at the manufacturing index subset (does not include utilities and mining):

Yes, we are still far below the peak, but the pattern of recovery remains firmly intact. There are not even signs of wheezing at this moment.

Thursday, May 13, 2010

Why Does My Stock Give Me Heartburn?

A fundamental question that nearly all investors have asked at one point or another or even still ask after many years in the market: Why does my stock bounce all over the place? All stocks are volatile to some extent because the overall market is volatile, but some are much moreso than others. Why does this happen?

There is no simple answer to this, but there is a basic framework that drives volatility in individual stocks and it can also be applied to the broader market as well in particular circumstances. The basic framework is along the following lines:

1. Volume levels (What % of shares outstanding trade in a given day?)

2. Earnings certainty (How stable are projected earnings?)

3. Previous volatility (Investor expectations are heavily based on the past. If a stock has been volatile in the past, investors assume it will be volatile in the future and this becomes a self-fulfilling prophecy)

Volume is a major factor for determining the stability of stocks. While low volumes do not necessitate that every day will be an adventure, they do make a stock more vulnerable to large moves. The basic logic is that if a stock only trades 50,000 shares a day, one huge buy order or one huge sell order can have huge sway over the course of the stock because generally there is not enough liquidity to absorb a large spike. However, if, say, a large buy or sell order hits Walmart (WMT), the high level of volume in Walmart shares will moderate that movement and prevent aberrant moves because the market's opinion of where the price of Walmart should be is much more developed than for, say, Consolidated Graphics (CGX). Broadly speaking, this dynamic means that larger companies will be less subject to volatility, but it is slightly more complicated than that. Some large stocks are more volatile than small companies for other reasons, two of which are listed below.

There is no simple answer to this, but there is a basic framework that drives volatility in individual stocks and it can also be applied to the broader market as well in particular circumstances. The basic framework is along the following lines:

1. Volume levels (What % of shares outstanding trade in a given day?)

2. Earnings certainty (How stable are projected earnings?)

3. Previous volatility (Investor expectations are heavily based on the past. If a stock has been volatile in the past, investors assume it will be volatile in the future and this becomes a self-fulfilling prophecy)

Volume is a major factor for determining the stability of stocks. While low volumes do not necessitate that every day will be an adventure, they do make a stock more vulnerable to large moves. The basic logic is that if a stock only trades 50,000 shares a day, one huge buy order or one huge sell order can have huge sway over the course of the stock because generally there is not enough liquidity to absorb a large spike. However, if, say, a large buy or sell order hits Walmart (WMT), the high level of volume in Walmart shares will moderate that movement and prevent aberrant moves because the market's opinion of where the price of Walmart should be is much more developed than for, say, Consolidated Graphics (CGX). Broadly speaking, this dynamic means that larger companies will be less subject to volatility, but it is slightly more complicated than that. Some large stocks are more volatile than small companies for other reasons, two of which are listed below.

Asset Allocation: A Dynamic Model

There are many approaches to asset allocation and I will try to give them all justice in turn. However, as promised, I will unveil one approach that I worked on for several months designed to pull off a difficult task: Picking the precise moments to shift in and out of stocks.

The model relies on three basic indicators:

1. The spread between earnings yield on the S&P 500 Index and the yield on 10-year Treasury Bonds

2. The spread between 10-year Treasury Bond rates and 90-day T-bills (one measure of the slope of the yield curve)

3. The spread between AAA rated corporate bonds and 10-year Treasury Bonds

For the uninitiated, earnings yield is calculated in the following way for an individual stock:

(1/PE ratio)*100% = earnings yield

For example on a 25 PE: (1/25)*100% = 4% earnings yield

The basic logic for each indicator being included is as follows:

1. The earnings yield spread is a measure of the relative valuation between stocks and bonds. A wide spread indicates that stocks are undervalued while an inverted spread indicates that stocks are overvalued.

2. The yield curve measurement relies on the predictive power of the Treasury yield curve for predicting major economic cycles. A heavily upwardly sloped yield curve indicates that the market expects short rates to rise in the near term because economic growth, and therefore inflation expectations, will be rising. An inverted yield curve indicates the opposite.

3. The corporate credit spread measurement is a proxy for financial panic and complacency. A wide spread indicates that markets are skittish and investors will only buy corporate bonds at severe discounts to Treasuries. A narrow spread indicates the opposite. This is a contrarian indicator. It is specified to give favorable signals when things look frightening for corporate credit.

Without getting into too many specifics at this point, the model relies on a composite score of the three indicators to give signals of when to re-balance your portfolio. The more favorable the composite becomes, the more you should shift into stocks. The more it indicates unfavorable conditions the more you should shift into bonds. Fairly simple, though the calculations were a pain.

The model has upper and lower bounds for asset allocation of 80% and 20% meaning that neither stocks or bonds can ever be less than 20% of your portfolio. I may respecify this to allow for 100% allocations, but I am not sold on that idea yet.

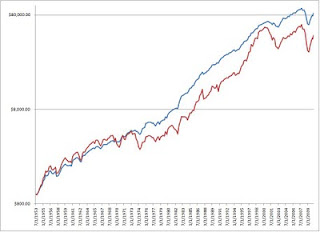

Here's a chart of how one specification of this model allocates:

It may look very volatile, but bear in mind this is over 57 years and it is crunched into a single graph.

It may look very volatile, but bear in mind this is over 57 years and it is crunched into a single graph.

Now, the fundamental question is: How does this work in practice? Does it provide a high rate of return with high rates of stability?

Well, historically back tested it produces a compounded annual growth rate of 8.0% vs 7.0% for an all-stock portfolio over the same period. More importantly, it does this with a lower range of volatility. The annual standard deviation for returns is 8.6% for the model and 15.3% for an all stock portfolio. Graphically, it looks something like this (red line is all stocks, blue line is the model under the specification above):

The graph is in logarithmic terms because it provides a more accurate picture. As you can see, the model is still prone to some losses in severe market downturns, but on the whole it is more stable.

One challenge of the model is that it is subject to long periods of under-performance like any balanced portfolio. The trick to the model is that it makes up a lot of ground in bear markets because it correctly moves investors into a bond-heavy position just before major declines. It does move back into stocks too soon in 2008, but it does have investors fully invested at the bottom and in for the subsequent rally. In the bear markets of 2000-2002, 1990, 1981-82, and 1973-74 it performs very well indeed.

Of course, the future might not look anything like the past, but I think such an approach is promising.

What do you all think?

Btw, the model currently suggests an 80-20 stock/bond split.

The model relies on three basic indicators:

1. The spread between earnings yield on the S&P 500 Index and the yield on 10-year Treasury Bonds

2. The spread between 10-year Treasury Bond rates and 90-day T-bills (one measure of the slope of the yield curve)

3. The spread between AAA rated corporate bonds and 10-year Treasury Bonds

For the uninitiated, earnings yield is calculated in the following way for an individual stock:

(1/PE ratio)*100% = earnings yield

For example on a 25 PE: (1/25)*100% = 4% earnings yield

The basic logic for each indicator being included is as follows:

1. The earnings yield spread is a measure of the relative valuation between stocks and bonds. A wide spread indicates that stocks are undervalued while an inverted spread indicates that stocks are overvalued.

2. The yield curve measurement relies on the predictive power of the Treasury yield curve for predicting major economic cycles. A heavily upwardly sloped yield curve indicates that the market expects short rates to rise in the near term because economic growth, and therefore inflation expectations, will be rising. An inverted yield curve indicates the opposite.

3. The corporate credit spread measurement is a proxy for financial panic and complacency. A wide spread indicates that markets are skittish and investors will only buy corporate bonds at severe discounts to Treasuries. A narrow spread indicates the opposite. This is a contrarian indicator. It is specified to give favorable signals when things look frightening for corporate credit.

Without getting into too many specifics at this point, the model relies on a composite score of the three indicators to give signals of when to re-balance your portfolio. The more favorable the composite becomes, the more you should shift into stocks. The more it indicates unfavorable conditions the more you should shift into bonds. Fairly simple, though the calculations were a pain.

The model has upper and lower bounds for asset allocation of 80% and 20% meaning that neither stocks or bonds can ever be less than 20% of your portfolio. I may respecify this to allow for 100% allocations, but I am not sold on that idea yet.

Here's a chart of how one specification of this model allocates:

Now, the fundamental question is: How does this work in practice? Does it provide a high rate of return with high rates of stability?

Well, historically back tested it produces a compounded annual growth rate of 8.0% vs 7.0% for an all-stock portfolio over the same period. More importantly, it does this with a lower range of volatility. The annual standard deviation for returns is 8.6% for the model and 15.3% for an all stock portfolio. Graphically, it looks something like this (red line is all stocks, blue line is the model under the specification above):

The graph is in logarithmic terms because it provides a more accurate picture. As you can see, the model is still prone to some losses in severe market downturns, but on the whole it is more stable.

One challenge of the model is that it is subject to long periods of under-performance like any balanced portfolio. The trick to the model is that it makes up a lot of ground in bear markets because it correctly moves investors into a bond-heavy position just before major declines. It does move back into stocks too soon in 2008, but it does have investors fully invested at the bottom and in for the subsequent rally. In the bear markets of 2000-2002, 1990, 1981-82, and 1973-74 it performs very well indeed.

Of course, the future might not look anything like the past, but I think such an approach is promising.

What do you all think?

Btw, the model currently suggests an 80-20 stock/bond split.

A United (?) Kingdom

So the Tories are back in power! And the Lib Dems are part of the coalition?

Whatever your political leanings, I think there is consensus that this is a strange alliance. And I think that this will have implications for the UK stock market.

For the sake of being bold, below is my hypothesis, please add your comments to it!

I predict that this coalition will last around two years and that we will see another UK election around summer of 2012. I think that David Cameron and Nick Clegg will actually personally get along, but they are closer aligned than their parties. So this points to a rather quick dissolution of the coalition. The reason I am giving them two years is that I think since both parties have been out of power for so long, they will not be eager to leave. But eventually, things will build up (I think it is likely that the Tories will not follow through on election reform) and the party base will get upset.

Second prediction is that this will be the new norm for the next several (maybe 4-6???) years. I think that the Lib Dems are on the rise and that Labour is on the way out. But, I'm not sure there will be a clean switch, instead I think this could be the start of some major three way action.

Why does any reader of this blog care? Normally I am pretty dismissive of the effect of so called "political turmoil" and its effects on the stock market (think about the big effect the Dems were suppose to have in 2006 or 2008), but I do think this UK election is significant since I really believe that there are now three viable parties in the UK. And this comes at a time when debt levels in UK are rising. I don't think any party will have the power (or the will) to make the tough decisions coming up... and I think the UK's economy will suffer.

Alex's Conclusion: Avoid too much exposure to the UK over the next several years!

Wednesday, May 12, 2010

Adventures around the World

Well, this will be my first post and then most likely my last post until the end of July. I will be traveling around the world: first a month in China and then three weeks in Europe.

Why does Finance Monitor care? Well, I can be our first investigative journalist! I will do my best to keep my eyes open for unique companies as well as seeing the depth to which international companies have penetrated the far reaches of the earth.

For example, when I visited China in 2008, I learned that Western toilets were a huge deal. The Chinese were (maybe still are?) transitioning from pit toilets to what we would call toilets. And the company to get a toilet with? Kohler! Too bad they are private...

So here is a list of places I will be in China (most likely flying, so these will be the only places):

Shanghai

Chengdu

Hong Kong

And in Europe the big cities are (with car and train travel between them):

London

Glasgow

Paris

Brussels

Amsterdam

So questions for everyone:

1. Any international company you want me watch for?

2. Any Chinese or European company I should look into?

3. What else should I look for?

Strategy Sessions- Part 1: Overview of Asset Allocation Versus Individual Securities

Steve brought up an interesting fundamental debate that investors have to resolve in their own heads: Should I be a stock picker or should I focus on asset allocation?

To put my own chips on the table here, I do both. Yes, it's a cop-out, but at the same time there is some value in it. Spreading your bets around not only different securities, not only around different asset classes, but even among different strategies does reduce the possibility of catastrophic loss and that is one of the chief objectives that any individual must bear in mind when making investments. Part of the reason I pick individual securities is that it simply keeps me interested in the market. The other reason is that I firmly believe that, with a good research methodology based on the fundamental value of companies, you can beat the market. However, I made my peace with the idea that I will not always beat the market and a lot of people do not come to terms with that.

As to the issues regarding picking individual securities, you must have a stomach of steel to handle the volatility. I own upwards of 18 different stocks at any one time so a large move in any one of them does not usually phase me. However, this sort of environment is not appropriate for many people for any number of reasons. Quite frankly, there is nothing wrong with being uncomfortable with high levels of volatility. It's a natural human reaction. If you do not feel able to keep up with the pace of the market, I would recommend broader strategies that focus more on asset allocation. Quite frankly, there is a damn good chance you will actually do better than being a trader or a stock picker. There's a great deal of evidence from economists and financial historians to support that idea.

To that end, I have devised a dynamic asset allocation tool designed to allocate into appropriate levels of stocks and bonds based on credit market indicators. The basic theory is that credit markets give indications of when you should get in and out of the market. I have always believed, with substantial empirical research from countless economists to support this belief, that interest rates are vital market signals and that relationships between different interest rates and those interest rates versus equity prices can be valuable investing tools. The model I have worked on will need revision as time goes on, but I think the general premise is solid.

In a few future posts related to this broader subject I will:

1. Discuss the dynamic asset allocation model introduced here

2. Outline some reasons why some individual stock holdings may be more subject to volatility than others

3. Introduce some methods for reducing volatility while still leaving open possibilities for gains

4. Whatever else I might think of

I'm doing this somewhat backwards because I am actually somewhat giddy to share the dynamic asset allocation model.

To put my own chips on the table here, I do both. Yes, it's a cop-out, but at the same time there is some value in it. Spreading your bets around not only different securities, not only around different asset classes, but even among different strategies does reduce the possibility of catastrophic loss and that is one of the chief objectives that any individual must bear in mind when making investments. Part of the reason I pick individual securities is that it simply keeps me interested in the market. The other reason is that I firmly believe that, with a good research methodology based on the fundamental value of companies, you can beat the market. However, I made my peace with the idea that I will not always beat the market and a lot of people do not come to terms with that.

As to the issues regarding picking individual securities, you must have a stomach of steel to handle the volatility. I own upwards of 18 different stocks at any one time so a large move in any one of them does not usually phase me. However, this sort of environment is not appropriate for many people for any number of reasons. Quite frankly, there is nothing wrong with being uncomfortable with high levels of volatility. It's a natural human reaction. If you do not feel able to keep up with the pace of the market, I would recommend broader strategies that focus more on asset allocation. Quite frankly, there is a damn good chance you will actually do better than being a trader or a stock picker. There's a great deal of evidence from economists and financial historians to support that idea.

To that end, I have devised a dynamic asset allocation tool designed to allocate into appropriate levels of stocks and bonds based on credit market indicators. The basic theory is that credit markets give indications of when you should get in and out of the market. I have always believed, with substantial empirical research from countless economists to support this belief, that interest rates are vital market signals and that relationships between different interest rates and those interest rates versus equity prices can be valuable investing tools. The model I have worked on will need revision as time goes on, but I think the general premise is solid.

In a few future posts related to this broader subject I will:

1. Discuss the dynamic asset allocation model introduced here

2. Outline some reasons why some individual stock holdings may be more subject to volatility than others

3. Introduce some methods for reducing volatility while still leaving open possibilities for gains

4. Whatever else I might think of

I'm doing this somewhat backwards because I am actually somewhat giddy to share the dynamic asset allocation model.

Sunday, May 9, 2010

German Regional Elections and Their Consequences

It pays to follow results such as these when we are in the middle of a crisis. Whatever you think of Angela Merkel, the rout of her party and its coalition partners in the North Rhine-Westphalia regional elections might spell deepened trouble for financial markets this coming week. Her government's backing for the bailout package for Greece seems to have a lot to do with these election results. As such, continued sovereign intervention in the European financial crisis appears doubtful. This is especially true as the most recent election result in the United Kingdom still has not produced a definitive outcome, and whatever coalition government emerges will be too weak to take on something as unpopular as bailing out fragile southern European economies.

Stay tuned and keep your eyes peeled. This may have already been anticipated by financial markets, but one cannot be sure.

Update: It appears given market futures that this is not having a huge impact on the markets and that they are instead focusing on the larger than expected responses by the EU and ECB in the last 24 hours. I'm glad to see that Jean Claude Trichet lost out and that the ECB will be providing assistance to governments should they be shut out of the private bond markets. His prior unwillingness was the cause of the Thursday and Friday blood baths.

Stay tuned and keep your eyes peeled. This may have already been anticipated by financial markets, but one cannot be sure.

Update: It appears given market futures that this is not having a huge impact on the markets and that they are instead focusing on the larger than expected responses by the EU and ECB in the last 24 hours. I'm glad to see that Jean Claude Trichet lost out and that the ECB will be providing assistance to governments should they be shut out of the private bond markets. His prior unwillingness was the cause of the Thursday and Friday blood baths.

Saturday, May 8, 2010

Economic Data Summary: Week Ending May 7th, 2010

This was an unambiguously positive week for economic data. If you don't have a lot of time on your hands, take that much from this post. Nearly every single indicator is moving in the right direction and most are improving in a big way.

As before, I will provide a brief description of why the data set is important if I have not covered it before.

April Employment Report

Bureau of Labor Statistics Link

For the uninitiated, this is arguably the most widely watched economic indicator and the one with the greatest impact on markets. What's nice about it is that the Bureau of Labor Statistics releases the data for the previous month within no more than 9 days of its completion and sometimes as little as 2. It is thus very timely and of very broad scope. Timeliness and scope are the two major factors that give an economic report its market moving potential.

Importantly, remember that the unemployment rate and the headline number of job creation are derived from two different series. The unemployment rate is derived from the Household Survey of employment, which is a monthly survey of approximately 30,000 households. The Establishment Survey is used to determine the number of non-farm payrolls created or lost in the course of a month. This is a survey of north of 300,000 employers covering a huge chunk of total employment. As such, the non-farm payrolls number is the more accurate as well as the more important of the two. The unemployment rate is an interesting talking point, but is not necessarily an accurate snapshot at any given time of labor force utilization, regardless of what measure you use.

So what happened in April? 290,000 non-farm payrolls were created and the unemployment rate edged up from 9.7% to 9.9%. Job gains were also revised up in March and February. The slight increase in the unemployment rate has to do with job seekers becoming encouraged by labor market conditions and returning to the labor force. The several hundred thousand if not millions who exited the labor force during the prior two years kept unemployment from rising more and will also keep it from falling too rapidly as jobs start coming back.

Gains were very widespread with the diffusion index for employers shooting up well over 60 at 64.3. This is well within the range of a healthy economic expansion, indicating far more employers are adding jobs than cutting them. Really impressive is how much manufacturing is coming back with 79,000 jobs created there in just the last three months. Of course, losses in manufacturing were enormous during the pit of the recession such as in April of last year when 149,000 jobs were lost, but this is a good sign. All major categories also gained jobs.

Now, I think the most important figure from a macroeconomic perspective is the aggregate weekly hours index. The reason is that this indicates what is the total amount of work happening in the economy. Theoretically, weekly hours could be declining while payrolls are rising and vice versa. As such, aggregate weekly hours is the best indicator of demand for labor. It has also risen substantially from the bottom last year :

Importantly, this is recovering far more rapidly than it has in the prior two recessions. Those expecting the slow "jobless recovery" that we got used to recently might, I will emphasize "might", be surprised.

April ISM Manufacturing and Non-Manufacturing Surveys

ISM Manufacturing Survey Link

ISM Non-Manufacturing Survey Link

For those who remember the post on the Chicago PMI and regional Federal Reserve indexes, these are the same sort of survey based diffusion indices. There is relatively little more to add to them except to say that they have much more sway on the market. The ISM manufacturing index in particular has historically had one of the most dramatic impacts on market movements of any indicator. This is because it is a national survey of manufacturing that is released on the first trading day of the month for the prior month. Manufacturing is the best leading indicator of the economy as a whole and the survey comes out right after the month is over. The non-manufacturing index is conducted in the same way, but even though it covers a larger sector of the economy it has a shorter history (only has been conducted since 1997) and seemingly worse tracking to the overall economy.

The ISM manufacturing index registered at a very strong 60.4%, indicating a very strong rate of expansion in manufacturing. Importantly, the new orders index came in at 65.7% with 52% reporting better orders and only 8% reporting lower orders. Put simply, this is beyond strong and indicates continued moderate to high rates of overall economic growth over the next few months at least.

The non-manufacturing index came in at 55.4%, which is fairly solid. The business activity index rose to a whopping 60.3% with 39% reporting higher activity and only 10% lower activity. Employment was a little weak, but the monthly employment report out of BLS contradicts this.

March Construction Spending

Census Bureau Construction Spending Link

This is pretty self-explanatory. It represents annualized outlays on private non-residential, private residential, and public construction projects. As it trails by more than a full month, it does not have particularly much market impact.

In March, spending rose by 0.2%, but this was driven almost entirely by public expenditures. Private non-residential and residential outlays fell by 0.7% and 1.1% respectively. Construction outlays have proven to be a continued source of weakness and non-residential in particular is unlikely to recover any time soon.

Jobless Claims

DOL Jobless Claims Link

Claims fell a little to 444,000, but they had been upwardly revised for the prior week. The level of jobless claims is proving stubbornly high, but it doesn't seem to be correlating with weakness in the labor markets. If this level correlates with what we saw in April's employment report, then it is good news, but this has clearly become harder to interpret.

April Car Sales, Personal Income and Spending, and April Chain Store Sales

Car sales in April were down a little from March as incentives were reduced, but still are on a recovery track. That said, at an 11.2 million annual rate, these are still very low levels of car sales.

Personal income and spending for March you would think would be a more closely followed report, but it really doesn't tell us much we didn't know already due to more timely indicators. Nonetheless, both income and spending showed strength in March. Spending was mainly bolstered by depleted savings and government transfer payments, so the trends of March will be difficult to repeat for long. However, with employment growth resuming, the "quality", for lack of a better term, of future consumption growth will likely improve. Link

April chain store sales were weak due to both bad weather in certain parts of the country and, more importantly, the shift of the Easter holiday. When the Census Department releases its Retail Sales report next week we will get a better sense of it. Normally these reports have a large influence on the markets due to their timeliness, but this week it was hard to tell due to the strangeness of Thursday.

Anyway, these and other reports are summarized on the Bloomberg Calendar

As before, I will provide a brief description of why the data set is important if I have not covered it before.

April Employment Report

Bureau of Labor Statistics Link

For the uninitiated, this is arguably the most widely watched economic indicator and the one with the greatest impact on markets. What's nice about it is that the Bureau of Labor Statistics releases the data for the previous month within no more than 9 days of its completion and sometimes as little as 2. It is thus very timely and of very broad scope. Timeliness and scope are the two major factors that give an economic report its market moving potential.

Importantly, remember that the unemployment rate and the headline number of job creation are derived from two different series. The unemployment rate is derived from the Household Survey of employment, which is a monthly survey of approximately 30,000 households. The Establishment Survey is used to determine the number of non-farm payrolls created or lost in the course of a month. This is a survey of north of 300,000 employers covering a huge chunk of total employment. As such, the non-farm payrolls number is the more accurate as well as the more important of the two. The unemployment rate is an interesting talking point, but is not necessarily an accurate snapshot at any given time of labor force utilization, regardless of what measure you use.

So what happened in April? 290,000 non-farm payrolls were created and the unemployment rate edged up from 9.7% to 9.9%. Job gains were also revised up in March and February. The slight increase in the unemployment rate has to do with job seekers becoming encouraged by labor market conditions and returning to the labor force. The several hundred thousand if not millions who exited the labor force during the prior two years kept unemployment from rising more and will also keep it from falling too rapidly as jobs start coming back.

Gains were very widespread with the diffusion index for employers shooting up well over 60 at 64.3. This is well within the range of a healthy economic expansion, indicating far more employers are adding jobs than cutting them. Really impressive is how much manufacturing is coming back with 79,000 jobs created there in just the last three months. Of course, losses in manufacturing were enormous during the pit of the recession such as in April of last year when 149,000 jobs were lost, but this is a good sign. All major categories also gained jobs.

Now, I think the most important figure from a macroeconomic perspective is the aggregate weekly hours index. The reason is that this indicates what is the total amount of work happening in the economy. Theoretically, weekly hours could be declining while payrolls are rising and vice versa. As such, aggregate weekly hours is the best indicator of demand for labor. It has also risen substantially from the bottom last year :

Importantly, this is recovering far more rapidly than it has in the prior two recessions. Those expecting the slow "jobless recovery" that we got used to recently might, I will emphasize "might", be surprised.

April ISM Manufacturing and Non-Manufacturing Surveys

ISM Manufacturing Survey Link

ISM Non-Manufacturing Survey Link

For those who remember the post on the Chicago PMI and regional Federal Reserve indexes, these are the same sort of survey based diffusion indices. There is relatively little more to add to them except to say that they have much more sway on the market. The ISM manufacturing index in particular has historically had one of the most dramatic impacts on market movements of any indicator. This is because it is a national survey of manufacturing that is released on the first trading day of the month for the prior month. Manufacturing is the best leading indicator of the economy as a whole and the survey comes out right after the month is over. The non-manufacturing index is conducted in the same way, but even though it covers a larger sector of the economy it has a shorter history (only has been conducted since 1997) and seemingly worse tracking to the overall economy.

The ISM manufacturing index registered at a very strong 60.4%, indicating a very strong rate of expansion in manufacturing. Importantly, the new orders index came in at 65.7% with 52% reporting better orders and only 8% reporting lower orders. Put simply, this is beyond strong and indicates continued moderate to high rates of overall economic growth over the next few months at least.

The non-manufacturing index came in at 55.4%, which is fairly solid. The business activity index rose to a whopping 60.3% with 39% reporting higher activity and only 10% lower activity. Employment was a little weak, but the monthly employment report out of BLS contradicts this.

March Construction Spending

Census Bureau Construction Spending Link

This is pretty self-explanatory. It represents annualized outlays on private non-residential, private residential, and public construction projects. As it trails by more than a full month, it does not have particularly much market impact.

In March, spending rose by 0.2%, but this was driven almost entirely by public expenditures. Private non-residential and residential outlays fell by 0.7% and 1.1% respectively. Construction outlays have proven to be a continued source of weakness and non-residential in particular is unlikely to recover any time soon.

Jobless Claims

DOL Jobless Claims Link

Claims fell a little to 444,000, but they had been upwardly revised for the prior week. The level of jobless claims is proving stubbornly high, but it doesn't seem to be correlating with weakness in the labor markets. If this level correlates with what we saw in April's employment report, then it is good news, but this has clearly become harder to interpret.

April Car Sales, Personal Income and Spending, and April Chain Store Sales

Car sales in April were down a little from March as incentives were reduced, but still are on a recovery track. That said, at an 11.2 million annual rate, these are still very low levels of car sales.

Personal income and spending for March you would think would be a more closely followed report, but it really doesn't tell us much we didn't know already due to more timely indicators. Nonetheless, both income and spending showed strength in March. Spending was mainly bolstered by depleted savings and government transfer payments, so the trends of March will be difficult to repeat for long. However, with employment growth resuming, the "quality", for lack of a better term, of future consumption growth will likely improve. Link

April chain store sales were weak due to both bad weather in certain parts of the country and, more importantly, the shift of the Easter holiday. When the Census Department releases its Retail Sales report next week we will get a better sense of it. Normally these reports have a large influence on the markets due to their timeliness, but this week it was hard to tell due to the strangeness of Thursday.

Anyway, these and other reports are summarized on the Bloomberg Calendar

Friday, May 7, 2010

Where/how to buy/sell?

I have a mutual fund that I have been putting a small amount of money into over the past 1.5 years. The transaction happens automatically every month and was setup through a financial planner that I was using at the time because I didn't know where to start. Because of this, I lose a small amount of the investment every month to fees, maybe something like 1%. I am looking to reduce or eliminate this loss. I may also be looking to buy individual stocks which the financial planner doesn't do.

I have looked at a few different online trading sites, but never really got a good feel for any of them. How is everyone else here buying and selling?

Thursday, May 6, 2010

Today's Ridiculous Performance and Lessons From It

I had the misfortune of being at a very boring series of presentations when all hell broke loose today, but I've read enough about it now to make some comments on it.

Whenever you are going through a period of market stress like we are, the market is vulnerable to truly massive daily swings. It's similar to setting off a firecracker behind someone suffering a panic attack. Today, there were some, to put it bluntly, bullshit trades that rapidly sold off major issues such as Procter and Gamble by ridiculous amounts. Just in case you don't know, P&G at one point today fell from $62 a share to $39 a share on absolutely no news whatsoever. On a stock with 2.9 billion shares, that erases $67 billion in market value in an instant. When a stalwart like P&G drops that much, many programmed trades will be slated to sell as well largely because that big of a drop in P&G leads to a major decline in the DJIA and S&P 500.